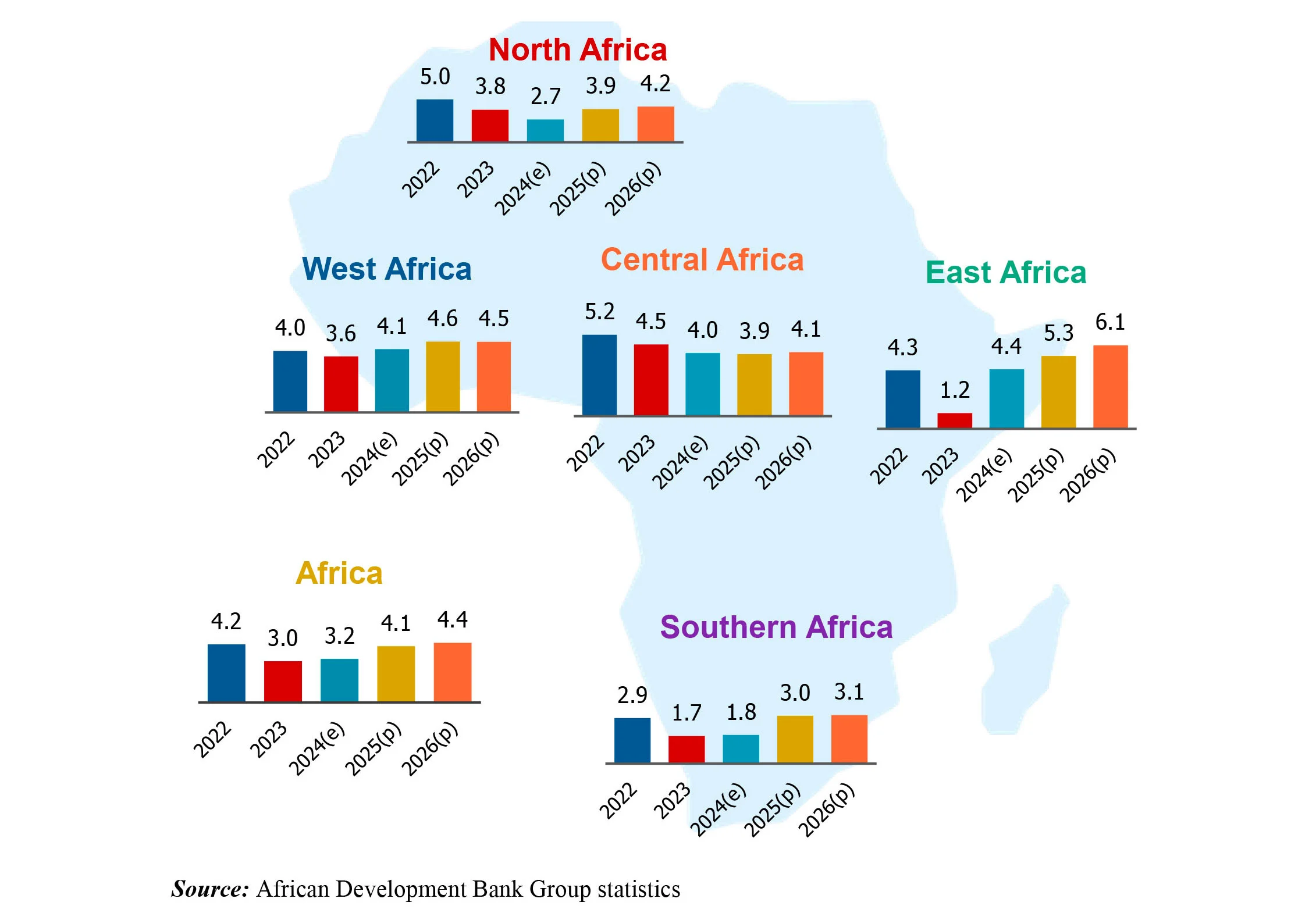

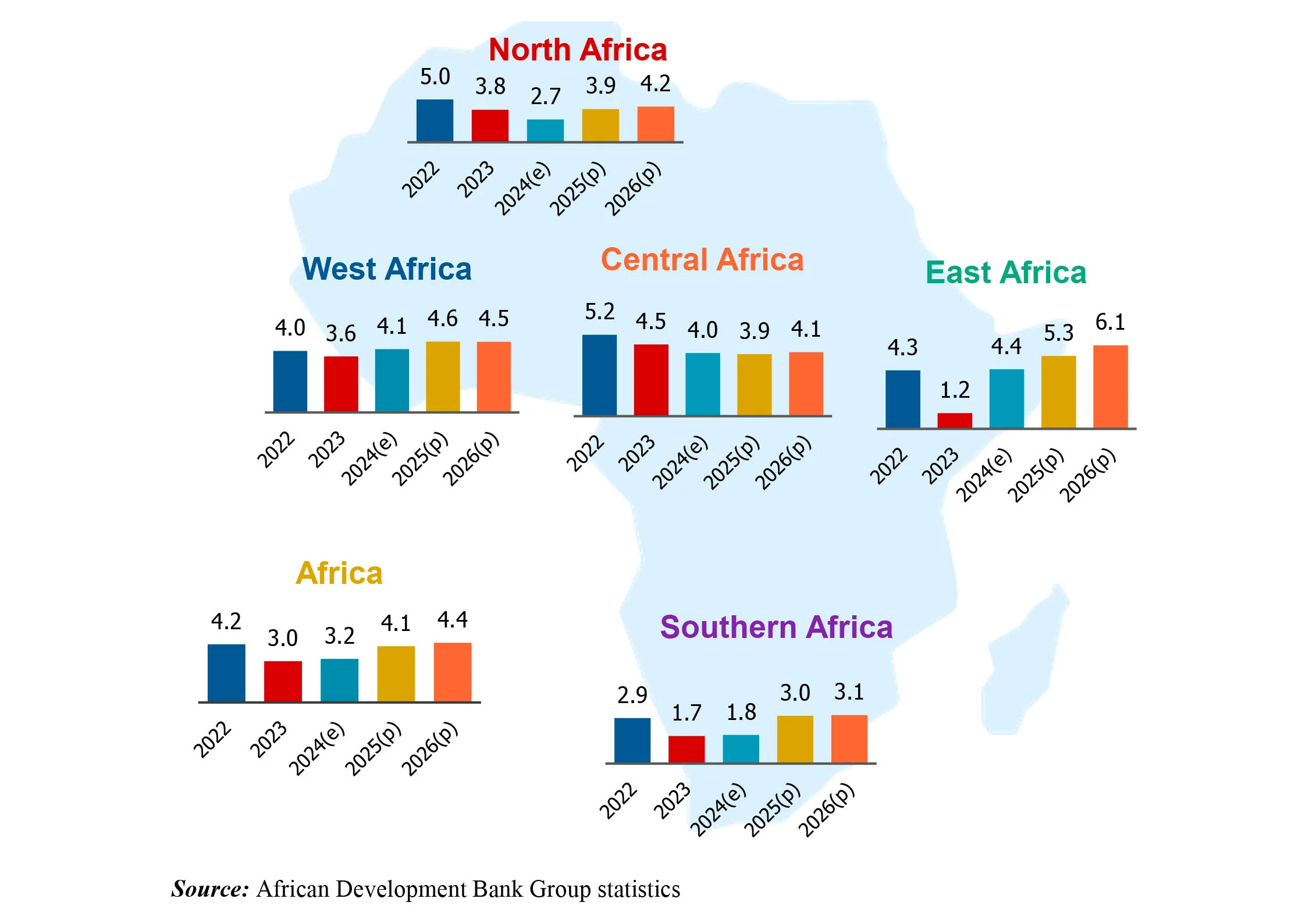

Africa will grow faster this year than every region on Earth except Asia. That fact gets repeated so often it's become background noise. But underneath the continental average of 4.1% GDP growth in 2025 sits one of the widest growth spreads in the world: Senegal near 8%, South Africa barely above stall speed at 1%, and a youth population entering the labor force faster than almost any job market on the planet can absorb it.

GDP & Growth Trends

The IMF projects 4.1% average real GDP growth across Africa in 2025, keeping the continent second globally behind Asia. Broken out by region:

- East Africa leads: Rwanda 7.1%, Ethiopia 6.6% (one source says 7.5%).

- West Africa close behind: Senegal 8.4%, Côte d'Ivoire 6.3–6.9% (carrying real cocoa-price-volatility risk).

- Southern Africa is the drag: South Africa at just 1.0%.

- North Africa is mixed: Egypt recovering to 4.3–5.0%.

Inflation is moderating toward 5.6–8.7% continentally, though Angola still runs above 22% YoY, and roughly 14 nations are flagged at high risk of debt distress. Monetary policy is diverging sharply — some banks holding rates high, Egypt already easing — meaning "Africa rates" isn't a single trade.

Population & Demographics

(Built from public UN/AfDB data — no site source exists.) Africa's population sits at roughly 1.5 billion, on track for ~2.5 billion by 2050 — the only major region where the working-age population is still expanding. Median age is around 19, versus a global median in the low 30s. This cuts two ways: a genuine "demographic dividend" if productively employed, but also the structural driver behind the youth-unemployment problem below. Urbanization is reshaping where growth concentrates (Lagos, Nairobi, Cairo, Accra, Kigali) and is the underlying enabler of the digital-economy growth described later.

Labor Market & Unemployment

Sources disagree: 21.0% youth unemployment (2023) vs. 22.4% (2025, described as a 1.8pp improvement). The honest takeaway: unemployment sits in the low-to-mid twenties, moving slowly in the right direction against a growing youth population. Structural findings: AfCFTA is only ~18% implemented (the single biggest unrealized lever here); ~600 million Africans lack reliable electricity; ~65% of curricula are misaligned with labor-market needs; SME financing shortfall estimated at ~$140 billion. A large informal-sector reality understates headline unemployment everywhere — for many young Africans, a smartphone and mobile wallet are the actual labor-market entry point.

Digital Economy & E-Commerce

Fintech/AI-driven services contribute an estimated 18% of Africa's GDP growth in 2025; the digital economy overall is valued around $180 billion, with mobile money transaction volume projected above $1.2 trillion. Recognizable names: Jumia, Safaricom's M-Pesa, Flutterwave, MTN, Vodacom. No article on the site ranks e-commerce platforms or B2B marketplaces despite visible search demand for exactly that — a real content gap.

Outlook & Investment Implications

Three scenarios recur: best case — digital leapfrogging adds $1.4 trillion to cumulative GDP by 2030; baseline — growth continues ~4.3% but inequality widens; downside — debt distress in 5+ nations forces austerity. Risk factors to monitor: climate shocks (40% of nations facing severe drought/flooding risk), global monetary policy spillover, China-linked commodity exposure (~28% in key mineral economies), and election-cycle volatility (19 national votes). Positioning ideas: favor domestic-demand sectors over pure commodity plays, hedge currency exposure, and don't ignore diaspora remittances (~$95 billion annually).

What This Means for You

- Allocating capital: treat "Africa" as a regional index, not a single risk — underwrite at the country level.

- Market-entry planning: check AfCFTA, power access, and skills pipelines before assuming labor supply solves staffing.

- Currency/rate pricing: monetary policy is diverging sharply — don't apply a single Africa-wide view.

- Digital-economy evaluation: the fintech story is real; treat company-level valuations as unverified until checked.

- Content/research planning: the biggest visible gap is e-commerce platforms/B2B marketplaces.

For a deeper briefing on how these divergences apply to a specific market or investment thesis, reach out to Annan Quaye's advisory team — a focused conversation is usually enough to figure out whether the opportunity fits.